Atlantic Sapphire - too big to fail?

Atlantic Sapphire photo.

I landed on this topic for a blog post after reading about the sale by Blue Future Holding (EW Group) of all their holdings in Atlantic Sapphire (approximately 4% of the company) and then having a long discussion with a fish farming crony about perspectives on salmon aquaculture in North America. During the conversation, my pal stated that Atlantic Sapphire was too big to fail and the value of the production licenses and capital investments made, would make it attractive for investors to weather the storm and see it through to a successful conclusion. I am skeptical of this kind of thinking but figured I should look at some of their reports and see if the numbers support that conclusion or if I am just a miserable, suspicious person.

I will preface this post by saying that I don’t have access to insider information and have not spoken to any of the team at Atlantic Sapphire or Blue Future Holding. I have, however, been following the development of this business for years and paid more than a normal amount of attention to its development as their very skillful efforts in raising investment capital were used to great effect by opponents of net pen farming to convince politicians that land-based farms were successful and viable.

A short history

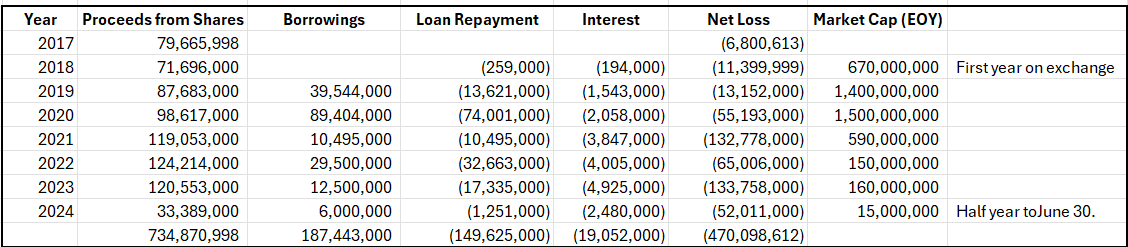

Atlantic Sapphire was listed on the Oslo stock exchange in 2018 and was extremely effective in raising capital, securing loan financing and building investor enthusiasm through masterful public relations efforts. This chart shows the history of share capital etc. over the past few years in USD. (Finance people – don’t @me – I’m not an accountant)

Key production figures from financial statements

In short, the founders raised $734m US, borrowed $187m US (repaid much of it), paid $19m in interest and had net losses of $470m US since 2017. My way of thinking would put the approximate value remaining in the company at $280m US – assuming the net loss figure accounts for depreciation, write-offs, operational losses etc. (I might be double-counting interest in this approach, which would add another $20m US)

This number tracks the mid-year balance sheet for Atlantic Sapphire which puts the value of property, plants and equipment at $274m US and the water rights and permits at $1.7m US.

Market Capitalization

Yesterday’s (8/26/2024) market cap for Atlantic Sapphire was $10m US which, on the surface of it, is a nonsensical valuation representing less than 3% of the likely asset value, and a tiny fraction of the peak 2020 valuation of $1.5b US. By the same token, the peak valuation of $1.5b was ridiculously high for a company that had produced less than 1,000 mt of salmon. I think this valuation demonstrated the extent to which stock market investors can be mislead by overly optimistic media coverage and the promise of glory. A harsh, and perhaps unfair comparison to the insanity around cryptocurrencies might not be out of line for a company that has performed this poorly. At least in terms of market performance.

Operational Performance

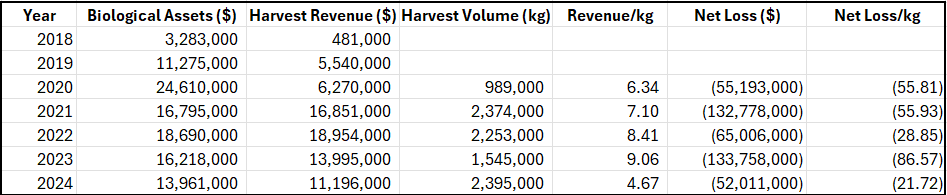

Unlike cryptocurrency traders, the team at Atlantic Sapphire have been trying to build a valuable physical asset. It just hasn’t gone well to this point. Here is a summary of their operational performance since 2018.

Key operational metrics

I’ve left out 2018 & 2019, as I couldn’t find some of the data for those years.

I’m sure their teams have learned a tremendous amount over the past few years, and I know they have some very good people working in the operation, but they clearly haven’t figured things out, or they are coming up against structural water quality or fish health issues that they can’t resolve in the short term. A few key points I take from this data:

Harvest volume

With a peak production of less than 2,500 metric tonnes over the past 5 years and what appears to be an emergency harvest in the first half of 2024 (given the incredibly low price achieved per kilo) suggests, to me, that their system currently can’t support anywhere near the biomass it was designed for. The initial plan for phase 1 was to produce 10,000 metric tons but, looking at the numbers, the experience suggests it can handle 1,000 – 1,500 tons.

Biological assets

It’s a limited data set but their largest net losses have followed years where they attempted to ramp up their biological asset base (2020 and 2022). The loss incurred in the first half of 2024 suggests, to me, that they were on pace to record another massive loss had they maintained their plan for the year. I’m not sure their press release tells the full story, but it was probably a good idea to take the pain now.

Production cost

A clumsy calculation puts their average production cost in the past 5 years at $56.89/kg with a peak at $95/kg in 2023 and the lowest point at $26/kg in the first half of this year. To put this in perspective, Grieg’s operating loss for the second quarter of 2024 was $2.3 NOK/kg ($0.21/kg US) and this was considered a disastrous result for them. With their best result, Atlantic Sapphire have produced an operational result that is about 100 times worse than a disastrous result for a competitor.

Too big to fail?

Getting back to the original intent of this article, the thesis my friend expressed was based on four key points:

1) The production permits in place for the facility have strategic value – they were likely incredibly hard to secure and won’t easily be replaced by a new entrant

2) The market is desperate for increased production of farmed salmon

3) The cost of airfreight into the US will only increase over time and increase the cost advantage of a domestic producer

4) So much has been invested in the Miami facility that it must have a long-term value

My comments on these points:

Production permits

They only have a value if they can demonstrate a productive value. So far, Atlantic Sapphire have not proven they can maintain a level of production anywhere near their plan. Perhaps there is value in their water rights? In Idaho, for example, the water rights owned by trout producers are worth far more than the value of their farming operations.

Market need

100% correct on this one. The US market simply can’t get enough salmon and there are significant barriers to growth in supply. The @Liberal Party of Canada is determined to kill 50% of the supply coming from Canada and European producers have lots of easier options than shipping to the US.

Air freight

Again 100% correct. The cost of air freight gives domestic producers a significant cost advantage over imports. Flying fillets into Miami likely costs Chilean producers $1.50/kg. The production cost for net pen producers is somewhere around $6.00/kg, so a domestic producer can likely compete at $7.50/kg (or thereabouts). The best result from Atlantic Sapphire is 3x this number.

Long-term value

I think the jury is still out on this one. The departure of a key investor, Blue Future Holdings, is a worrying sign, as is their need to raise another $90m US on top of the $734m they have already spent. In aquaculture circles, these are mind-bending numbers, but you don’t have to dig too deep to find similar losses leading to bankruptcy in other sectors. A key challenge with a facility designed for Atlantic salmon is that it may not be suitable for another species or type of operation. A few years ago, I looked at a land-based salmon farm with the idea of converting it into a smolt production facility. In that case, the layout of the facility would have required such extensive redesign that an acquisition made no sense. If the system can’t produce Atlantic salmon sustainably and needs extensive investment to make it suitable for something else, you could end up with a stranded asset and a disposal problem.

Conclusion

Farming salmon is hard and 1000% harder if you are trying to do something new and at scale like Atlantic Sapphire. Net pen raised farmed salmon currently spend ~40% of their life span in land-based facilities and it can be tempting to draw the conclusion that it shouldn’t be too hard to extend to the full cycle on land. With net pen production, though, the biomass carried in land-based systems represents roughly 10% of the total biomass produced. The challenge of producing the additional 90% in a land-based system is several orders of magnitude harder than doing it in the sea.

I think the founders and investors deserve all the credit in the world for the boldness of their vision and the resources and determination they have put behind the project but, to this point, the arrows are still not pointing in the right direction to convince me that the company is too big to fail.

If you are still reading at this point, thank you very much. Comments, feedback, corrections can be directed to Info@AlanWCook.com or via LinkedIn.